ShowRisk - Prediction of Credit Risk

by Gerhard Paaß

The growing number of insolvencies as well as the intensified international competition calls for reliable procedures to evaluate the credit risk (risk of insolvency) of bank loans. GMD has developed a methodology that improves the current approaches in a decisive aspect: the explicit characterization of the predictive uncertainty for each new case. The resulting procedure does not only derive a single number as result, but also describes the uncertainty of this number.

Credit Scoring procedures use a representative sample to estimate the credit risk, the probability that a borrower will not repay the credit. If all borrowers had the same features, the credit risk may be estimated. Therefore the uncertainty of the estimate is reduced if the number of sample elements grows. In the general case complex models (eg neural networks or classification trees) are required to capture the relation between the features of the borrowers and the credit risk. Most current procedures are not capable to estimate the uncertainty of the predicted credit risk.

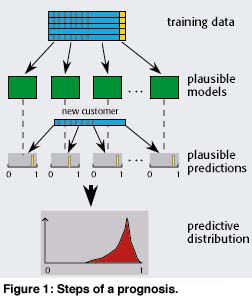

Prediction with Plausible Models

We employ the Bayesian theory to generate a representative selection of models describing the uncertainty. For each model a prediction is performed which yields a distribution of plausible predictions. As each model represents another possible relation between inputs and outputs, all these possibilities are taken into account in the joint prediction.

A theoretical derivation shows that the average of these plausible predictions in general has a lower error than single ‘optimal’ predictions. This was confirmed by an empirical investigation: For a real data base of several thousand enterprises with more than 70 balance sheet variables, the GMD procedure only rejected 35.5% of the ‘good’ loans, whereas other methods (neural networks, fuzzy pattern classification, etc.) rejected at least 40%.

Expected Profit as Criterion

The criterion for accepting a credit is a loss function specifying the gain or loss in case of solvency/insolvency. Using the predicted credit risk we may estimate the average or expected profit. According to statistical decision theory a credit application should be accepted if this expected profit is positive. Depending on the credit conditions (interest rate, securities) this defines a decision threshold for the expected profit.

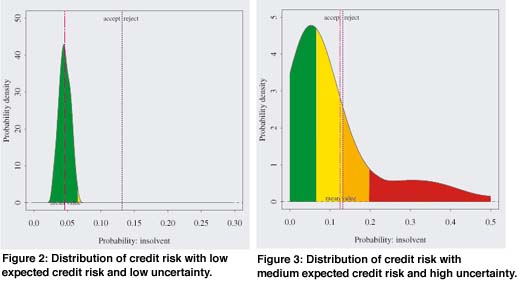

In figures 2 and 3 the decision threshold for a credit condition is depicted: If the predicted average credit risk is above the threshold, a loss is to be expected on average and the loan application should be rejected. Figure 2 shows a predictive distribution where the expected credit risk is low. The uncertainty about the credit risk is low, too, and the loan application could be accepted without further investigations. The expected credit risk of the predictive distribution in figure 3 is close to the decision threshold.

The actual credit risk could be located in the favourable region the intermediate range or in the adverse region. The information in the training data are not sufficient to assign the credit risk to one of the regions. Obviously the data base contains too few similar cases for this prediction resulting in an uncertain prediction. Therefore in this case there is a large chance that additional information, especially a closer audit of the customer, yields a favorable credit risk.

Application

Under a contract the credit scoring procedure was adapted to the data of the German banking group Deutscher Sparkassen und Giroverband and is currently in a test phase. For each new application it is possible to modify the credit conditions (interest rate, securities) to find the conditions, where the credit on the average will yield a profit. For a prediction the computing times are about a second. Currently an explanation module is developed which will explain the customer and the bank officer in terms of plausible rules and concepts, why the procedure generated a specific prediction.

Please contact:

Gerhard Paaß - GMD

Tel: +49 2241 14 2698

E-mail: paass@gmd.de